Perovskite Photovoltaic Materials Engineering Market Report 2025: In-Depth Analysis of Breakthroughs, Growth Drivers, and Global Opportunities. Explore Key Trends, Forecasts, and Strategic Insights Shaping the Industry.

- Executive Summary and Market Overview

- Key Technology Trends in Perovskite Photovoltaic Materials (2025–2030)

- Competitive Landscape and Leading Players

- Market Growth Forecasts and Revenue Projections (2025–2030)

- Regional Analysis: Market Dynamics by Geography

- Challenges, Risks, and Barriers to Adoption

- Opportunities and Strategic Recommendations

- Future Outlook: Innovation Pathways and Market Evolution

- Sources & References

Executive Summary and Market Overview

Perovskite photovoltaic materials engineering represents a rapidly advancing segment within the solar energy sector, characterized by the development and optimization of perovskite-structured compounds for use in high-efficiency solar cells. As of 2025, the global market for perovskite photovoltaics is experiencing robust growth, driven by the material’s potential to deliver higher power conversion efficiencies at lower production costs compared to traditional silicon-based photovoltaics. Perovskite materials, typically hybrid organic-inorganic lead or tin halide-based compounds, have demonstrated laboratory efficiencies exceeding 25%, rivaling and in some cases surpassing established photovoltaic technologies.

The market landscape is shaped by significant investments in research and development, with both established energy companies and innovative startups accelerating the commercialization of perovskite solar cells. According to International Energy Agency, the global solar PV market is projected to continue its double-digit growth, with perovskite technologies expected to capture a growing share due to their scalability and compatibility with flexible and tandem cell architectures. The ability to manufacture perovskite cells using low-temperature solution processes further enhances their appeal for large-scale deployment and integration into building materials, portable devices, and next-generation solar modules.

- Market Size and Growth: The perovskite photovoltaic market is forecasted to reach a valuation of over USD 2 billion by 2025, with a compound annual growth rate (CAGR) exceeding 30% from 2022 to 2025, as reported by MarketsandMarkets.

- Key Players: Leading organizations such as Oxford PV, Saule Technologies, and GCL System Integration Technology are at the forefront of scaling up perovskite cell production and advancing engineering solutions to address stability and toxicity challenges.

- Technological Advancements: Recent breakthroughs in encapsulation, tandem cell integration, and lead-free perovskite formulations are accelerating the path to commercialization and regulatory approval, as highlighted by National Renewable Energy Laboratory.

In summary, perovskite photovoltaic materials engineering is poised to transform the solar energy market in 2025, offering a compelling combination of efficiency, versatility, and cost-effectiveness. The sector’s trajectory will be shaped by continued innovation, strategic partnerships, and the successful navigation of technical and regulatory hurdles.

Key Technology Trends in Perovskite Photovoltaic Materials (2025–2030)

Perovskite photovoltaic materials engineering is poised for significant advancements between 2025 and 2030, driven by the need to overcome stability, scalability, and efficiency challenges. The focus is shifting from laboratory-scale breakthroughs to industrially viable solutions, with several key technology trends emerging.

- Stability Enhancement: One of the most critical engineering challenges is improving the long-term operational stability of perovskite solar cells. Recent research emphasizes compositional engineering, such as the incorporation of mixed cations (e.g., formamidinium, cesium) and halides, to mitigate phase segregation and moisture sensitivity. Encapsulation techniques using advanced barrier materials are also being refined to protect perovskite layers from environmental degradation, a trend highlighted in recent reports by the National Renewable Energy Laboratory (NREL).

- Scalable Manufacturing Processes: Transitioning from spin-coating to scalable deposition methods—such as slot-die coating, blade coating, and inkjet printing—is a major engineering focus. These techniques enable uniform, large-area film formation compatible with roll-to-roll manufacturing, which is essential for commercial deployment. Companies like Oxford PV are pioneering pilot lines that demonstrate the feasibility of these processes at scale.

- Interface and Layer Engineering: Engineering the interfaces between perovskite absorbers and charge transport layers is crucial for minimizing recombination losses and enhancing device efficiency. Innovations include the use of self-assembled monolayers, 2D/3D perovskite heterostructures, and passivation strategies to suppress defect states, as detailed in recent publications from the Helmholtz-Zentrum Berlin.

- Lead-Free and Low-Toxicity Alternatives: Environmental and regulatory concerns are driving research into lead-free perovskite compositions, such as tin-based and double perovskite materials. While these alternatives currently lag behind in efficiency, engineering efforts are focused on improving their optoelectronic properties and stability, as noted by the International Energy Agency (IEA).

- Tandem Integration: Perovskite-silicon tandem cells are a major engineering trend, with perovskite layers being optimized for compatibility with silicon bottom cells. This includes tuning bandgaps, optimizing layer thicknesses, and developing robust interconnection schemes. First Solar and other industry leaders are investing in tandem architectures to push efficiencies beyond the single-junction limit.

These engineering trends are expected to define the competitive landscape of perovskite photovoltaics through 2030, as the industry moves toward commercialization and large-scale deployment.

Competitive Landscape and Leading Players

The competitive landscape of perovskite photovoltaic materials engineering in 2025 is characterized by rapid innovation, strategic partnerships, and a race to commercialize high-efficiency, stable perovskite solar cells. The sector is marked by a blend of established photovoltaic companies, specialized startups, and academic spin-offs, all vying for technological leadership and market share.

Key players include Oxford PV, widely recognized for its pioneering work in perovskite-silicon tandem cells, which have achieved record-breaking efficiencies exceeding 29%. The company’s close ties with the University of Oxford and its robust intellectual property portfolio have positioned it as a frontrunner in scaling up perovskite technology for commercial deployment. Another major contender is Microquanta Semiconductor, a Chinese firm that has made significant strides in large-area perovskite module production and outdoor stability, targeting both utility-scale and building-integrated photovoltaics.

In the United States, U.S. Department of Energy Solar Energy Technologies Office has funded several initiatives, supporting companies like Silicon Perovskite Inc. and TandemPV Inc., both of which are developing scalable manufacturing processes and addressing long-term stability challenges. These efforts are complemented by European consortia such as imec, which collaborates with industrial partners to integrate perovskite layers into existing silicon cell production lines, aiming for cost-effective mass production.

Startups like Solliance and GCL System Integration are also notable for their focus on flexible and lightweight perovskite modules, targeting niche applications such as portable power and building facades. Meanwhile, major materials suppliers, including Merck Group, are investing in the development of high-purity perovskite precursors and encapsulation materials to enhance device longevity and manufacturability.

The competitive environment is further shaped by ongoing collaborations between academia and industry, as well as by government-backed research programs in Asia, Europe, and North America. As the field moves toward commercialization, the leading players are those able to demonstrate not only high efficiency but also scalable production, long-term stability, and compliance with environmental standards.

Market Growth Forecasts and Revenue Projections (2025–2030)

The perovskite photovoltaic materials engineering market is poised for robust growth in 2025, driven by accelerating advancements in material stability, efficiency, and scalable manufacturing processes. According to projections by IDTechEx, the global perovskite solar cell market is expected to transition from pilot-scale production to early commercialization in 2025, with revenues anticipated to surpass $200 million for the year. This growth is underpinned by increasing investments from both established photovoltaic manufacturers and new entrants, particularly in Asia and Europe, where government-backed initiatives are fostering rapid technology adoption.

Key drivers for 2025 include the successful demonstration of perovskite-silicon tandem cells with efficiencies exceeding 28%, as reported by National Renewable Energy Laboratory (NREL). These breakthroughs are expected to catalyze demand for engineered perovskite materials that offer improved moisture resistance and operational lifetimes, addressing previous barriers to commercialization. As a result, material suppliers specializing in encapsulation, interface engineering, and scalable ink formulations are projected to see double-digit revenue growth in 2025.

- Asia-Pacific: The region is forecasted to lead in perovskite photovoltaic materials engineering revenue, with China and South Korea ramping up pilot lines and early-stage mass production. According to Wood Mackenzie, Chinese manufacturers are expected to account for over 40% of global perovskite module output in 2025.

- Europe: The European Union’s Green Deal and Horizon Europe programs are channeling significant funding into perovskite R&D, with several demonstration projects scheduled for completion in 2025. This is expected to drive regional market revenues to approximately $60 million, as per IEA PVPS estimates.

- North America: While commercialization lags behind Asia and Europe, U.S.-based startups and research consortia are projected to secure increased venture capital and government grants, supporting a market revenue of $30 million in 2025 (U.S. Department of Energy).

Overall, the perovskite photovoltaic materials engineering sector is set for a pivotal year in 2025, with global revenues projected to grow by over 50% year-on-year, laying the foundation for exponential expansion through the remainder of the decade.

Regional Analysis: Market Dynamics by Geography

The regional dynamics of the perovskite photovoltaic materials engineering market in 2025 are shaped by a combination of policy frameworks, R&D investments, manufacturing capabilities, and end-user adoption rates across key geographies. The Asia-Pacific region, led by China, Japan, and South Korea, is expected to dominate market growth due to robust government support for renewable energy, significant investments in next-generation solar technologies, and a well-established electronics manufacturing ecosystem. China, in particular, is accelerating pilot-scale production and commercialization of perovskite solar cells, leveraging its supply chain advantages and state-backed initiatives to reduce carbon emissions (International Energy Agency).

Europe remains a critical hub for perovskite R&D, with the European Union funding multiple collaborative projects aimed at improving the stability and scalability of perovskite materials. Countries such as Germany, the United Kingdom, and Switzerland are home to leading research institutions and startups pioneering tandem cell architectures and roll-to-roll manufacturing processes. The EU’s Green Deal and ambitious solar deployment targets are expected to drive further investment and pilot deployments, particularly in building-integrated photovoltaics (BIPV) and flexible solar applications (European Commission).

In North America, the United States is witnessing increased venture capital activity and public-private partnerships focused on scaling up perovskite manufacturing and addressing durability challenges. The U.S. Department of Energy’s Solar Energy Technologies Office is funding initiatives to accelerate commercialization, while several universities and startups are advancing ink formulation and encapsulation techniques to meet local climate requirements (U.S. Department of Energy). However, the region faces competitive pressure from Asia in terms of cost-effective mass production.

Other regions, including the Middle East and Latin America, are in the early stages of perovskite adoption but are showing interest due to high solar irradiance and growing demand for decentralized energy solutions. Pilot projects in the United Arab Emirates and Brazil are exploring the integration of perovskite modules in utility-scale and off-grid applications (International Renewable Energy Agency).

Overall, regional market dynamics in 2025 will be defined by the interplay of innovation ecosystems, policy incentives, and the ability to transition from laboratory breakthroughs to commercial-scale deployment.

Challenges, Risks, and Barriers to Adoption

The engineering of perovskite photovoltaic materials, while promising for next-generation solar cells, faces several significant challenges, risks, and barriers to widespread adoption as of 2025. One of the most critical issues is the long-term stability of perovskite materials. Unlike traditional silicon-based photovoltaics, perovskite solar cells (PSCs) are highly sensitive to environmental factors such as moisture, oxygen, heat, and ultraviolet (UV) light. These sensitivities can lead to rapid degradation, limiting operational lifetimes and raising concerns about their commercial viability. Recent studies indicate that even with advanced encapsulation techniques, maintaining performance over 20-25 years—a standard for commercial solar panels—remains a formidable hurdle National Renewable Energy Laboratory.

Another major barrier is the presence of toxic lead in the most efficient perovskite formulations. Lead leakage during manufacturing, operation, or disposal poses environmental and health risks, potentially triggering regulatory restrictions. Although research into lead-free alternatives (such as tin-based perovskites) is ongoing, these materials currently lag behind in efficiency and stability International Energy Agency.

Scalability and reproducibility also present significant engineering challenges. Laboratory-scale perovskite cells have achieved impressive efficiencies, but translating these results to large-area modules with uniform quality and minimal defects is complex. Issues such as film uniformity, interface engineering, and defect passivation must be addressed to ensure consistent performance at scale. Manufacturing processes must also be compatible with existing industrial infrastructure to facilitate cost-effective mass production Wood Mackenzie.

Intellectual property (IP) fragmentation and a lack of standardized testing protocols further complicate the commercialization landscape. The rapid pace of innovation has led to a crowded IP space, making it difficult for new entrants to navigate licensing and patent issues. Additionally, the absence of universally accepted standards for testing perovskite module durability and performance creates uncertainty for investors and end-users IEA Photovoltaic Power Systems Programme.

Finally, market acceptance is hindered by the nascent track record of perovskite technology. Bankability, insurance, and financing for large-scale projects remain limited until long-term field data can demonstrate reliability and safety comparable to established PV technologies.

Opportunities and Strategic Recommendations

The perovskite photovoltaic materials engineering sector is poised for significant growth in 2025, driven by rapid advancements in material stability, scalability, and efficiency. As the industry transitions from laboratory-scale breakthroughs to commercial applications, several key opportunities and strategic recommendations emerge for stakeholders seeking to capitalize on this dynamic market.

- Commercialization of Tandem Solar Cells: Perovskite-silicon tandem cells have demonstrated power conversion efficiencies exceeding 30%, surpassing traditional silicon cells. Companies investing in tandem architectures can leverage this efficiency advantage to target premium segments such as utility-scale solar and building-integrated photovoltaics (National Renewable Energy Laboratory).

- Materials Innovation for Stability: Addressing the long-term stability of perovskite materials remains a top priority. Strategic partnerships with chemical suppliers and research institutions to develop robust encapsulation techniques and lead-free perovskite formulations can unlock new markets, especially in regions with stringent environmental regulations (International Energy Agency).

- Scaling Manufacturing Processes: Investment in scalable, low-cost manufacturing methods such as roll-to-roll printing and vapor deposition will be critical. Early movers in process engineering can achieve cost leadership and secure supply agreements with major solar module manufacturers (Wood Mackenzie).

- Geographic Expansion: Emerging markets in Asia-Pacific and Latin America present untapped opportunities due to rising energy demand and supportive policy frameworks. Strategic localization of production and partnerships with regional energy developers can accelerate market entry (International Renewable Energy Agency).

- Intellectual Property and Licensing: Building a robust IP portfolio around novel perovskite compositions and device architectures will be essential for long-term competitiveness. Licensing agreements and technology transfer partnerships can generate additional revenue streams and foster industry-wide adoption (World Intellectual Property Organization).

In summary, stakeholders should prioritize R&D in stability and scalability, pursue strategic alliances, and focus on geographic and segment diversification. Proactive engagement with regulatory bodies and investment in IP protection will further strengthen market positioning as perovskite photovoltaics move toward mainstream adoption in 2025.

Future Outlook: Innovation Pathways and Market Evolution

The future outlook for perovskite photovoltaic materials engineering in 2025 is marked by rapid innovation and a clear trajectory toward commercial viability. As the solar industry seeks alternatives to traditional silicon-based cells, perovskite materials are at the forefront due to their tunable bandgaps, high absorption coefficients, and potential for low-cost manufacturing. The next wave of innovation is expected to focus on three primary pathways: stability enhancement, scalable manufacturing, and tandem cell integration.

- Stability Enhancement: One of the most significant challenges for perovskite photovoltaics has been their susceptibility to moisture, heat, and UV degradation. In 2025, research is converging on compositional engineering—such as the incorporation of mixed cations and halides—to improve intrinsic material stability. Encapsulation technologies are also advancing, with new barrier films and hybrid organic-inorganic layers extending operational lifetimes to rival those of silicon cells. According to National Renewable Energy Laboratory, recent prototypes have demonstrated stable performance over 2,000 hours under accelerated aging conditions, a key milestone for commercial adoption.

- Scalable Manufacturing: Transitioning from lab-scale spin-coating to industrial-scale roll-to-roll and slot-die coating processes is a critical focus. In 2025, pilot lines are being established in Asia and Europe, leveraging inkjet and vapor deposition techniques to produce large-area modules with uniform quality. Oxford PV and Saule Technologies are leading efforts to scale up production, with the first commercial perovskite-silicon tandem modules expected to enter the market this year.

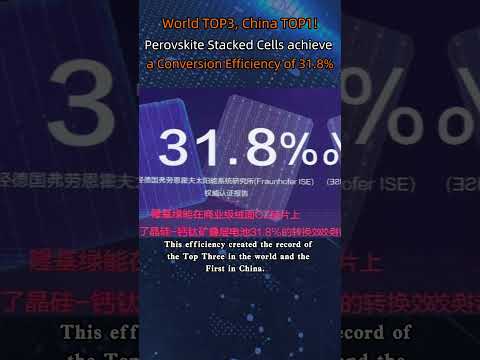

- Tandem Cell Integration: The integration of perovskite layers atop silicon or CIGS cells is a major innovation pathway, aiming to surpass the single-junction efficiency limits. In 2025, perovskite-silicon tandem cells have achieved certified efficiencies above 30%, as reported by Fraunhofer ISE. This leap in performance is driving interest from utility-scale solar developers and module manufacturers seeking to differentiate their offerings.

Looking ahead, the market evolution for perovskite photovoltaics is expected to accelerate, with global investments and partnerships intensifying. The International Energy Agency projects that perovskite-based modules could capture a significant share of new solar installations by the late 2020s, provided that ongoing engineering challenges are addressed and bankability is established (International Energy Agency). The coming year will be pivotal in determining the pace and scale of perovskite adoption in the broader photovoltaic market.

Sources & References

- International Energy Agency

- MarketsandMarkets

- Oxford PV

- Saule Technologies

- National Renewable Energy Laboratory

- Helmholtz-Zentrum Berlin

- First Solar

- Microquanta Semiconductor

- imec

- Solliance

- IDTechEx

- Wood Mackenzie

- European Commission

- World Intellectual Property Organization

- Fraunhofer ISE