Volumetric Video Broadcasting Industry Report 2025: Market Growth, Technology Innovations, and Strategic Insights for the Next 5 Years

- Executive Summary & Market Overview

- Key Technology Trends in Volumetric Video Broadcasting

- Competitive Landscape and Leading Players

- Market Growth Forecasts (2025–2030): CAGR, Revenue, and Adoption Rates

- Regional Analysis: North America, Europe, Asia-Pacific, and Rest of World

- Challenges, Risks, and Emerging Opportunities

- Future Outlook: Strategic Recommendations and Market Entry Points

- Sources & References

Executive Summary & Market Overview

Volumetric video broadcasting is an advanced media technology that captures, processes, and transmits three-dimensional spaces and subjects, enabling viewers to experience immersive, interactive content from any angle. Unlike traditional 2D video, volumetric video leverages arrays of cameras and depth sensors to reconstruct dynamic 3D models, which can be streamed in real time or on-demand to devices such as AR/VR headsets, smartphones, and web browsers. This technology is rapidly gaining traction across entertainment, sports, education, and enterprise sectors, driven by the proliferation of 5G networks, edge computing, and the growing consumer appetite for immersive experiences.

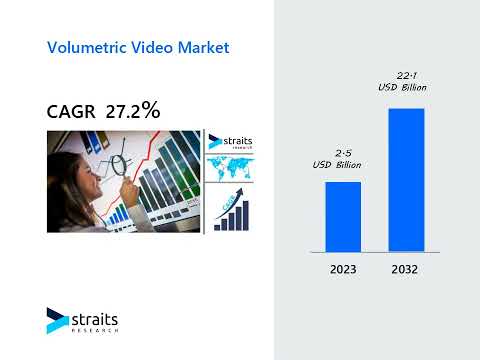

The global volumetric video broadcasting market is poised for significant growth in 2025. According to MarketsandMarkets, the volumetric video market is projected to reach USD 4.9 billion by 2025, expanding at a CAGR of over 26% from 2020. This surge is fueled by increasing investments from major technology companies, the expansion of content creation studios, and the integration of volumetric capture in live events and remote collaboration platforms.

Key industry players such as Microsoft, Intel, and 8i are pioneering volumetric capture and streaming solutions, while broadcasters and content creators are experimenting with new formats for sports, concerts, and interactive storytelling. The adoption of volumetric video in live sports broadcasting, for example, allows fans to view replays from any perspective, enhancing engagement and monetization opportunities for rights holders and sponsors.

Regionally, North America and Europe are leading the market, supported by robust R&D ecosystems and early adoption of immersive media technologies. However, Asia-Pacific is expected to witness the fastest growth, propelled by investments in 5G infrastructure and a burgeoning gaming and entertainment industry, as noted by Grand View Research.

Despite its promise, the market faces challenges such as high production costs, bandwidth requirements, and the need for standardized formats. Nevertheless, ongoing advancements in compression algorithms, cloud rendering, and AI-driven post-processing are expected to lower barriers and accelerate mainstream adoption. In summary, 2025 marks a pivotal year for volumetric video broadcasting, with expanding commercial deployments and a growing ecosystem of technology providers, content creators, and end-users.

Key Technology Trends in Volumetric Video Broadcasting

Volumetric video broadcasting is rapidly evolving, driven by advancements in capture, processing, and delivery technologies. In 2025, several key technology trends are shaping the landscape, enabling more immersive and interactive experiences across entertainment, sports, education, and enterprise applications.

- Real-Time Volumetric Capture and Processing: The shift toward real-time volumetric video is accelerating, with companies deploying multi-camera arrays and depth sensors capable of capturing dynamic 3D scenes at high frame rates. Innovations in GPU acceleration and edge computing are reducing latency, making live volumetric streaming increasingly viable. For example, Microsoft and Intel have both demonstrated real-time volumetric capture for live events.

- AI-Driven Compression and Reconstruction: The massive data generated by volumetric video requires advanced compression techniques. In 2025, AI-powered codecs and neural network-based reconstruction are significantly improving bandwidth efficiency without sacrificing quality. Nokia and Qualcomm are among the leaders leveraging machine learning to optimize volumetric video streams for both cloud and edge delivery.

- Standardization and Interoperability: Industry-wide efforts to standardize volumetric video formats and streaming protocols are gaining momentum. The Moving Picture Experts Group (MPEG) is advancing standards such as MPEG-I for immersive media, while the 3rd Generation Partnership Project (3GPP) is integrating volumetric video support into 5G and 6G specifications, facilitating broader adoption and cross-platform compatibility.

- Cloud-Native and Edge Delivery: The deployment of cloud-native volumetric video platforms is enabling scalable, on-demand processing and distribution. Edge computing is further reducing latency for interactive applications, particularly in gaming and live sports. Amazon Web Services (AWS) and Google Cloud are investing in infrastructure to support volumetric content delivery at scale.

- Device and Platform Integration: The proliferation of AR/VR headsets, smartphones, and web-based viewers is driving demand for seamless volumetric video playback. Cross-device compatibility and adaptive streaming are becoming standard, with platforms like Meta Quest and Apple Vision Pro supporting high-fidelity volumetric experiences.

These technology trends are collectively lowering barriers to entry, expanding creative possibilities, and setting the stage for volumetric video broadcasting to become a mainstream medium by 2025 and beyond.

Competitive Landscape and Leading Players

The competitive landscape of the volumetric video broadcasting market in 2025 is characterized by rapid innovation, strategic partnerships, and a growing number of specialized players. As demand for immersive content in entertainment, sports, education, and enterprise applications accelerates, both established technology giants and agile startups are vying for market share.

Key industry leaders include Microsoft, whose Mixed Reality Capture Studios have set benchmarks for high-fidelity volumetric capture, and Intel, which has invested heavily in volumetric video through its True View technology, widely adopted in live sports broadcasting. Sony has also entered the space, leveraging its imaging expertise to develop advanced volumetric capture solutions for both entertainment and industrial use cases.

Among specialized players, 8i and Yulio are notable for their focus on scalable, cloud-based volumetric video platforms, enabling real-time streaming and integration with AR/VR devices. Holoxica and Arcturus are recognized for their proprietary compression algorithms and editing tools, which address the significant data challenges inherent in volumetric video workflows.

Strategic collaborations are shaping the market, with companies like Verizon partnering with volumetric studios to leverage 5G networks for low-latency, high-bandwidth broadcasting. Similarly, T-Mobile has piloted volumetric video streaming for live events, highlighting the role of telecom operators in enabling next-generation broadcast experiences.

Geographically, North America and Europe remain the primary hubs for innovation and adoption, driven by the presence of leading technology firms and robust content ecosystems. However, Asia-Pacific is emerging as a significant growth region, with investments from companies like NTT Communications in Japan and Samsung in South Korea.

Overall, the 2025 market is marked by intense competition, with differentiation hinging on capture quality, real-time processing, compression efficiency, and seamless integration with existing broadcast and streaming infrastructures.

Market Growth Forecasts (2025–2030): CAGR, Revenue, and Adoption Rates

The volumetric video broadcasting market is poised for significant expansion between 2025 and 2030, driven by advancements in capture technology, increasing demand for immersive content, and the proliferation of 5G networks. According to projections by MarketsandMarkets, the global volumetric video market is expected to grow at a compound annual growth rate (CAGR) of approximately 28% during this period, with the broadcasting segment representing a substantial share of this growth. Revenue from volumetric video broadcasting is forecasted to surpass $3.5 billion by 2030, up from an estimated $900 million in 2025, as adoption accelerates across sports, entertainment, and live event sectors.

Adoption rates are expected to rise sharply as broadcasters and content creators seek to differentiate their offerings with interactive and immersive experiences. The integration of volumetric video into live sports broadcasts, for example, is anticipated to increase viewer engagement and open new monetization avenues through personalized content and advertising. Grand View Research highlights that North America and Europe will lead in early adoption, with Asia-Pacific markets following closely as infrastructure and consumer demand mature.

- Sports and Live Events: By 2027, over 30% of major sports broadcasts in North America are projected to incorporate volumetric video elements, according to Dell Technologies.

- Entertainment and Media: The entertainment sector is expected to account for nearly 40% of volumetric video broadcasting revenue by 2030, as studios and streaming platforms invest in next-generation content formats.

- Enterprise and Education: Adoption in enterprise training and educational broadcasting is forecasted to grow at a CAGR of 25% from 2025 to 2030, per International Data Corporation (IDC).

Key drivers for this growth include falling costs of volumetric capture hardware, improved real-time rendering capabilities, and the expansion of cloud-based processing solutions. However, challenges such as high initial investment and bandwidth requirements may temper adoption in some regions. Overall, the period from 2025 to 2030 is expected to mark a transformative phase for volumetric video broadcasting, with rapid revenue growth and increasing mainstream adoption across multiple industries.

Regional Analysis: North America, Europe, Asia-Pacific, and Rest of World

The global volumetric video broadcasting market is experiencing dynamic growth, with regional trends shaped by technological infrastructure, investment levels, and content innovation. In 2025, North America, Europe, Asia-Pacific, and the Rest of the World (RoW) each present distinct opportunities and challenges for market participants.

- North America: North America remains the frontrunner in volumetric video broadcasting, driven by robust R&D investments, a mature media ecosystem, and the presence of leading technology firms such as Microsoft and Intel. The U.S. market, in particular, benefits from early adoption in sports broadcasting, live events, and immersive advertising. According to Grand View Research, North America accounted for over 35% of global volumetric video revenues in 2024, with continued growth expected as 5G and edge computing infrastructure expand.

- Europe: Europe is characterized by strong government support for digital innovation and a vibrant creative sector. Countries like the UK, Germany, and France are investing in volumetric studios and cross-industry collaborations. The European Union’s digital strategy and funding initiatives, such as Horizon Europe, are accelerating adoption in cultural heritage, education, and live entertainment. Statista projects that the region will see a CAGR of over 25% through 2025, with increasing demand for localized content and interactive experiences.

- Asia-Pacific: The Asia-Pacific region is emerging as a high-growth market, fueled by rapid digitalization, a large consumer base, and government-backed smart city projects. Japan, South Korea, and China are leading in volumetric video R&D, with companies like Sony and Huawei investing in capture technology and cloud-based broadcasting. MarketsandMarkets forecasts that Asia-Pacific will register the fastest growth rate globally, driven by demand for immersive entertainment, esports, and virtual tourism.

- Rest of World (RoW): In regions such as Latin America, the Middle East, and Africa, adoption is at an earlier stage but gaining momentum. Infrastructure limitations and high costs remain barriers, but pilot projects in education, healthcare, and live events are underway. International partnerships and falling hardware prices are expected to accelerate uptake, with IDC noting a steady increase in volumetric video pilot deployments across emerging markets.

Overall, while North America and Europe currently lead in volumetric video broadcasting, Asia-Pacific’s rapid expansion and the gradual emergence of RoW markets are set to reshape the global landscape by 2025.

Challenges, Risks, and Emerging Opportunities

Volumetric video broadcasting, which enables the capture and transmission of three-dimensional spaces and subjects for immersive experiences, is poised for significant growth in 2025. However, the sector faces a complex landscape of challenges and risks, even as new opportunities emerge.

One of the primary challenges is the immense data volume generated by volumetric video. High-fidelity 3D capture can require gigabits per second of bandwidth, straining existing network infrastructure and making real-time broadcasting difficult, especially over mobile or consumer-grade connections. This bottleneck is compounded by the need for advanced compression algorithms that preserve quality without introducing latency or artifacts. While 5G and edge computing offer partial solutions, widespread adoption remains uneven globally, limiting market reach Ericsson.

Another significant risk is the high cost and complexity of volumetric capture systems. Studios require arrays of cameras, specialized lighting, and powerful processing hardware, resulting in substantial upfront investments. This restricts access to large media companies and well-funded enterprises, slowing the democratization of volumetric content creation. Additionally, interoperability issues persist, as there is no universal standard for volumetric video formats, complicating distribution across platforms and devices IDC.

Content security and privacy also present risks. Volumetric video can capture highly detailed personal likenesses and environments, raising concerns about unauthorized use, deepfakes, and data breaches. Regulatory frameworks are still evolving, and companies must navigate a patchwork of privacy laws and ethical considerations Gartner.

Despite these hurdles, emerging opportunities are driving investment and innovation. The proliferation of AR/VR headsets and spatial computing devices is expanding the addressable market for volumetric content, particularly in entertainment, sports, education, and remote collaboration. Advances in AI-driven compression, real-time rendering, and cloud-based processing are expected to lower technical barriers and costs. Furthermore, partnerships between technology providers, broadcasters, and telecom operators are accelerating the development of scalable volumetric broadcasting solutions Dell Technologies.

In summary, while volumetric video broadcasting in 2025 faces significant technical, economic, and regulatory challenges, the sector is also witnessing rapid innovation and expanding commercial opportunities, setting the stage for broader adoption in the coming years.

Future Outlook: Strategic Recommendations and Market Entry Points

The future outlook for volumetric video broadcasting in 2025 is shaped by rapid technological advancements, evolving content consumption habits, and increasing investments from both technology giants and media companies. As the market matures, strategic recommendations and market entry points become critical for stakeholders aiming to capitalize on emerging opportunities.

Strategic Recommendations:

- Invest in Scalable Infrastructure: The computational and bandwidth demands of volumetric video are significant. Companies should prioritize partnerships with cloud service providers and edge computing platforms to ensure seamless capture, processing, and delivery of high-fidelity 3D content. For example, Microsoft Azure and Google Cloud are expanding their offerings to support volumetric workflows.

- Focus on Interoperability and Standards: The lack of unified standards for volumetric video formats and streaming protocols remains a barrier. Industry players should actively participate in standardization initiatives, such as those led by the Moving Picture Experts Group (MPEG) and 3GPP, to ensure broad compatibility and accelerate adoption.

- Target High-Value Vertical Markets: Early adoption is most prominent in sports broadcasting, live events, education, and healthcare. Companies should tailor solutions for these sectors, leveraging case studies like Intel’s True View in sports and 8i in immersive education.

- Enhance User Experience: To drive mainstream adoption, focus on reducing latency, improving compression algorithms, and developing intuitive user interfaces for both VR/AR and traditional screens. Collaborations with device manufacturers such as Meta and Apple can help optimize content delivery for next-generation headsets.

Market Entry Points:

- Content Production Studios: Establishing or partnering with volumetric capture studios, like Dimension Studio, offers a direct route into the content creation ecosystem.

- Platform Development: Building or integrating with distribution platforms that support volumetric streaming, such as Holo-Light, can position new entrants as key enablers in the value chain.

- White-Label Solutions: Offering turnkey volumetric video solutions to broadcasters and event organizers can accelerate market penetration, especially in regions with limited in-house expertise.

In summary, the 2025 landscape for volumetric video broadcasting favors agile, collaborative, and technically robust strategies. Early movers who address infrastructure, standards, and user experience challenges will be best positioned to capture value as the market scales.

Sources & References

- MarketsandMarkets

- Microsoft

- Grand View Research

- Nokia

- Qualcomm

- Moving Picture Experts Group (MPEG)

- 3rd Generation Partnership Project (3GPP)

- Amazon Web Services (AWS)

- Google Cloud

- Meta Quest

- Apple Vision Pro

- Yulio

- Arcturus

- Verizon

- Dell Technologies

- International Data Corporation (IDC)

- Statista

- Huawei

- Dimension Studio